Popular credit cards

Cash back card

Earn up to 5% cash back

Rewards

$500 online cash rewards bonus offer & 5% cash back on your selected categories

1.5% cash back on all other eligible purchases

Annual Fee

No annual fee intro the first year

APR

0% Intro APR on purchases and any balance transfers within the first 2 month of your account opening

Business card

Earn up to 5% cash back

Rewards

$500 online cash rewards bonus offer & 5% cash back on your selected categories

1.5% cash back on all other eligible purchases

Annual Fee

No annual fee intro the first year

APR

0% Intro APR on purchases and any balance transfers within the first 2 month of your account opening

Fair credit card

Earn up to 5% cash back

Rewards

$500 online cash rewards bonus offer & 5% cash back on your selected categories

1.5% cash back on all other eligible purchases

Annual Fee

No annual fee intro the first year

APR

0% Intro APR on purchases and any balance transfers within the first 2 month of your account opening

More ways to user your credit card

Everyday purchases

Use your credit card for everyday expenses like groceries, gas, or utility bills. It provides a convenient payment option, and by paying your balance in full each month, you can avoid interest charges.

Rewards & cashback

Many credit cards offer rewards programs or cashback on eligible purchases. Take full advantage of these valuable benefits by strategically using your credit card for everyday expenses like groceries, gas, or utility bills.

Online shopping

Credit cards are frequently utilized for online transactions, offering an additional level of security via fraud protection services. Make sure to purchase from reputable websites and utilize secure payment gateways.

Debt collection

When using your credit card for transactions, it's important to be aware of debt collection processes. If you have outstanding balances, our bank or authorized agencies may contact you to discuss repayment options. We prioritize transparency and compliance with relevant regulations to ensure fair debt collection practices.

Manage your business credit

Leveraging your business credit card strategically involves utilizing its features to not only track expenses, earn rewards, and manage cash flow effectively but also to build a positive credit history, streamline financial reporting, and access credit when needed for business growth and opportunities.

Get credit card from 3 simple process

Getting a credit card typically involves a straightforward process that can be summarized in three simple steps:

Research and compare

Submit an application

Approval and activation

No overdraft Fees

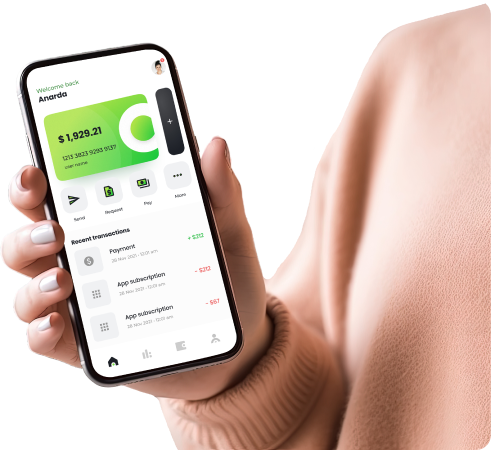

Do all your banking safely and conveniently through our mobile app